Amazon FBA Sellers with US LLC: Connection Risk, IRS Data Sharing, and Account-Linking Triggers (2026)

How Amazon detects related seller accounts (IP, device, payment, behavioral signals), what IRS data flows through 1099-K and W-8BEN-E, and the structural reality of running multiple stores under one or multiple US LLCs for non-resident sellers.

Key Takeaways

- Enforcement cascades downward through linked accounts.

- Track 1: Form 5472 (every year, regardless of Amazon activity).

Quick take

Key Takeaways

- Amazon's automated systems detect related seller accounts using IP address, device fingerprint, payment instruments, banking, business address, tax IDs, and behavioral patterns. A different LLC name is not by itself enough to break the link.

- Account-linking enforcement is asymmetric: a violation on one linked account can suspend all linked accounts, but creating a new account while a related account is under enforcement is treated as policy circumvention and can result in permanent closure across the network.

- Foreign-owned single-member US LLCs sit at the intersection of two reporting tracks: the IRS Form 5472 obligation for the LLC itself (every year, even with zero revenue) and Amazon's 1099-K / W-8BEN-E reporting that flows transaction data to the IRS.

- W-8BEN-E correctly filed by a foreign entity with no US trade or business changes the 1099-K treatment, but does not eliminate the structural visibility of the entity in IRS records via the W-8BEN-E itself.

- Multi-store strategies (separate LLCs per brand, separate LLCs per region) work structurally only when every linking signal is separated: separate IP, separate device, separate payment rails, separate business address, separate beneficial owner where the policy permits.

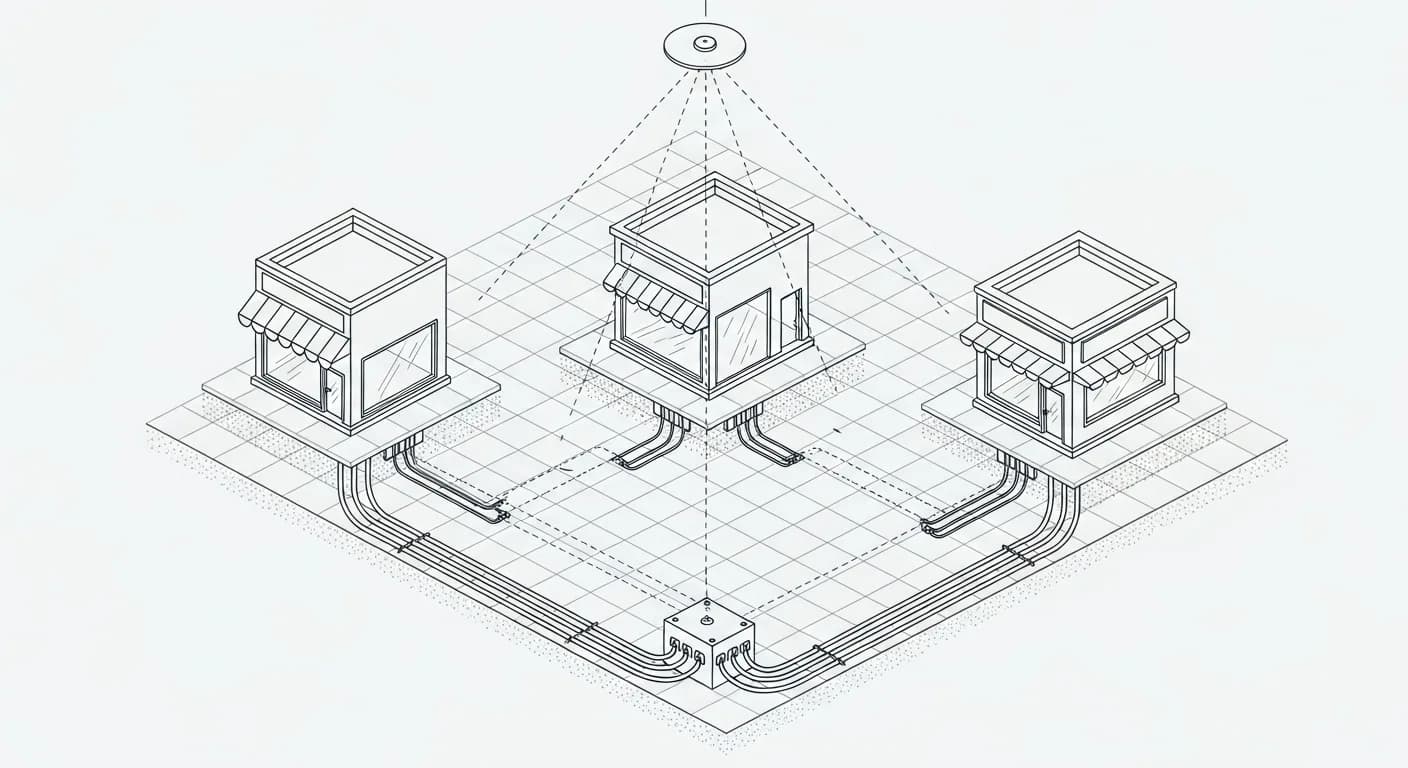

The Connection Problem

A non-resident seller forms a Wyoming LLC, opens an Amazon US seller account, ships products, builds a brand. A year later they want to add a second brand — different product category, different positioning, different audience. The intuitive instinct: form a second LLC, open a second Amazon account, run the two side by side.

Amazon's automated review systems treat the two as the same operator if even a few linking signals overlap. The second account opens, sells for a few months, and one day both accounts go to "Account Health" review simultaneously. A compliance issue on one cascades to the other. A "linked accounts" decision can result in both being suspended at the same time.

The structural reality: Amazon doesn't see entities. It sees patterns of access, payment, behavior, and identifiers. A different LLC name on the surface does not separate the underlying network in Amazon's view. Account linkage is a function of the operating environment, not the legal structure on paper.

How Amazon Detects Related Accounts

Amazon Seller Performance and Account Health teams use both automated systems and manual review. The signals automated systems weight most heavily across documented enforcement cases:

IP address. Logins from the same IP range, the same residential ISP, or the same VPN exit node link accounts. Sellers operating from outside the US who use VPNs to access seller central make this signal especially loud: many non-resident sellers route through the same handful of US-based VPN endpoints.

Device fingerprint. Browser configuration, screen resolution, installed fonts, time zone setting, and a long list of other client signals create a fingerprint that Amazon stores per session. Two seller accounts accessed from the same device share the fingerprint.

Payment instruments. A credit card, debit card, or bank account used to fund advertising or to receive disbursements that has previously been associated with another seller account creates a link. This is one of the most common causes of unintended linkage — a founder uses their personal credit card to advertise on Amazon for both stores, and the card itself ties the accounts.

Banking and disbursement. Seller disbursements going to the same bank account (Mercury, Wise Business, Payoneer, traditional bank) link the receiving accounts. See the Mercury vs Wise vs Relay analysis for the disbursement options available to non-resident sellers and the trade-offs between them.

Business address and registered agent. Two LLCs sharing the same registered agent address or the same business address create an inferred link. Wyoming LLCs are common among non-resident sellers, and most use one of a small number of registered agent services — so RA address alone is a weak signal, but combined with other signals it strengthens the case.

Tax ID. EIN and W-9 or W-8BEN-E identity information flowing to Amazon is logged. A founder who applies for multiple EINs as the responsible party leaves a record that Amazon's compliance team can correlate.

Behavioral signals. Listing patterns, supplier relationships (especially when invoices match), product variant overlap, and inventory shipping origin all factor in. Two accounts shipping from the same FBA prep center, using similar product photography, and listing similar SKUs are correlated even before any IP or device match.

The signals are weighted and combined. A single match (only same RA address) is often not enough to trigger automated linkage. A combination (same RA address + same Wise Business account + same device fingerprint) typically is.

How does your structure score?

Free 2-minute screening across Money, Entity, Tax, and Accountability.

What Account-Linking Enforcement Actually Looks Like

Two enforcement asymmetries matter:

Enforcement cascades downward through linked accounts. When Amazon's Account Health team identifies a violation on one account and links it to others, the others can be placed under review or suspended at the same time. The link is not bidirectional in obligation — the seller doesn't owe Amazon an explanation about the other accounts pre-emptively — but the enforcement action treats them as one operator.

Creating a new account to escape enforcement compounds the risk. Amazon's published policy treats opening a new account while a related account is under enforcement as "circumventing review." This typically results in the new account being detected at the linking layer, then permanently closed alongside the original. The "open a new account and start fresh" path is the most common compounding error in account suspension cases.

A different pattern matters when the seller wants to legitimately migrate (different business entity, different beneficial owner, genuinely separated operations): Amazon's published guidance is that the legal entity and country field cannot be changed within an existing account. The path is closure of the old account followed by opening a new account with the new credentials. The compliance question is whether the linking signals between old and new are sufficiently separated to avoid the automated link.

The IRS Data Path for Foreign-Owned LLC Amazon Sellers

The IRS reporting structure for non-resident Amazon sellers operating through a US LLC has two distinct tracks:

Track 1: Form 5472 (every year, regardless of Amazon activity). A foreign-owned single-member US LLC must file Form 5472 with a Pro Forma Form 1120 annually, reporting reportable transactions with foreign related parties. This obligation exists independent of any Amazon reporting. See Form 5472: The $25K penalty most LLC owners miss for the filing mechanics and what happens if Form 5472 is missed for the penalty structure.

Track 2: Amazon's reporting (1099-K or W-8BEN-E pathway). Amazon's tax reporting depends on which form the seller submits during account onboarding:

- W-9 (US person or US entity). Amazon reports payments via Form 1099-K when the seller crosses the reporting threshold for that tax year. The threshold has shifted several times: the American Rescue Plan Act set a $600 threshold, this was repeatedly delayed by the IRS through transition rules, and Congress reverted the threshold via the One Big Beautiful Bill Act (Public Law 119-21, signed July 4, 2025). The current reporting threshold as of the most recent IRS guidance is the pre-2022 level ($20,000 in gross payments and 200 transactions). Verify the current year's threshold against the IRS Form 1099-K guidance at the time of filing — the threshold has been a moving target.

- W-8BEN-E (foreign entity). A foreign-owned US LLC that submits a properly completed W-8BEN-E to Amazon — claiming foreign-owner status, no US trade or business under the relevant tax treaty, and the entity's foreign tax identification number where applicable — has different treatment. For sellers whose income is determined to be exempt from US tax reporting on this basis, Amazon does not issue a 1099-K. However, the W-8BEN-E itself is submitted to Amazon and stored in their records; Amazon retains both the W-8BEN-E and the underlying transaction data.

The critical point on the W-8BEN-E pathway: the absence of a 1099-K does not mean the entity is invisible to the IRS. The 5472 obligation under Track 1 continues regardless. The W-8BEN-E is itself a US tax form that documents the foreign-owner relationship and, if examined later, demonstrates exactly which foreign person owns the entity that received the Amazon disbursements.

The "Different Entity = Different Visibility" Misunderstanding

A pattern that appears in non-resident seller communities: form a second LLC under a different name with a different EIN, treating the new entity as structurally separate from the first. This breaks down on multiple layers:

On Amazon's side. The linking signals discussed above (IP, device, payment, banking, address) are unrelated to the legal name on the entity. A second LLC with a different EIN is treated as the same operator if any subset of those signals match.

On the IRS side. Two LLCs with two EINs filing two Form 5472s with the same foreign beneficial owner name produce two records pointing to the same person. The foreign owner appears on both Pro Forma 1120 packages as the related party. If one entity has a compliance gap, the IRS examining that gap sees the second entity through the related-party disclosure.

On the home-country side. For sellers in jurisdictions with CRS reporting (most of Europe, parts of Asia, including China — see CRS reporting and China's STA), the bank accounts holding both LLCs' funds report to the home-country tax authority. Two LLCs feeding into accounts that report under CRS surface as the same individual's offshore activity.

The structural separation that "second LLC for second store" implies on paper requires complete operational separation to hold up under Amazon's automated review or under tax examination. Most multi-store sellers operating from a single founder's setup do not achieve this separation in practice.

When a Suspension Cascades

The most common pattern for suspension cascades, observed in seller-community case write-ups:

- Account A receives a performance notification — late shipment, restricted product, suspected inauthentic complaint.

- Account A is placed under review.

- Within hours or days, Amazon's account linking systems flag account B as related.

- Account B receives the same review action, even though account B had no independent trigger.

- Both accounts are suspended pending appeal.

- The appeal for account A requires explaining the connection to account B and the operating reasons for the multi-store setup.

- If the explanation is consistent with Amazon's multiple-accounts policy (separate entities, separate operations, prior written approval where required), reinstatement may follow. If the explanation reveals undisclosed linkage, both accounts may be permanently closed.

The asymmetric risk: a perfect performance record on the new account does not protect it from cascade. The connection itself is the trigger, not the new account's behavior.

The Structural Questions Before Forming a Second LLC

For sellers considering a second Amazon account under a separate LLC, the structural questions that determine actual separation:

- Beneficial owner. Is the second LLC owned by a different person, or by the same foreign person? If the same, two layers of records (5472 + W-8BEN-E + CRS where applicable) still point to one operator.

- Operating environment. Will the two accounts be accessed from physically separate devices, on separate internet connections, with separate browser profiles? "Logged out of one, logged into the other" on the same machine does not separate the device fingerprint.

- Payment rails. Will the two LLCs have separate banking, separate credit cards used for advertising, separate beneficial owner on those payment instruments? Funds eventually distributing to the same foreign owner is structurally OK on the tax side, but the rails between Amazon and that distribution need to be separate.

- Suppliers and inventory. Are the two product lines genuinely different (different suppliers, different categories, different FBA shipments)? Two accounts sharing inventory or sharing a supplier invoice can be linked through behavioral signals even when payment and identity are separated.

- Amazon's policy permission. Amazon's official guidance is that operating multiple accounts requires a legitimate business need (different brand for different category, different country marketplace, etc.) and that selling the same products across multiple accounts is not permitted. The policy framework is published in Amazon's seller policies and changes periodically.

When the answer to most of these is "the same as the first LLC," the second LLC adds entity-level reporting burden (a second annual 5472 obligation, a second EIN, a second registered agent, a second state filing) without producing the separation the seller was trying to achieve.

Banking-Layer Considerations Specific to Amazon Sellers

The disbursement banking relationship is where Amazon-specific friction often shows up. Three patterns recur:

Mercury or Relay rejection at onboarding. Through 2025 and into 2026 Q1-Q2, both Mercury and Relay tightened non-resident application acceptance. Registered agent addresses are no longer accepted as the LLC's US address at either provider. Amazon FBA sellers whose only US presence is the formation paperwork now face higher rejection rates at the neobank layer. See the updated banking redundancy guidance and the Mercury vs Wise vs Relay comparison for the current state.

Wise Business as the practical Layer-2. For non-resident sellers, Wise Business is now the more common disbursement destination when Mercury or Relay are not accessible. Wise is not a US bank — it is an electronic money institution with safeguarded funds, not FDIC-insured — but Amazon disburses to Wise USD account details and the structure works operationally for many non-resident sellers.

Payoneer's marketplace-native option. Payoneer has been positioned in the marketplace-payouts segment for years, accepting Amazon disbursements directly with currency-conversion to local accounts (including conversion to RMB for Chinese sellers, INR for Indian sellers, etc.). See the Wise vs Payoneer vs Mercury comparison for the specific trade-offs.

The structural point: whichever banking layer receives the Amazon disbursement becomes a linking signal in Amazon's account-correlation system. If the same Wise account or the same Payoneer account receives disbursements from two different Amazon stores, the two stores are linked at the banking layer regardless of which LLC owns them.

When Account Review Surfaces Structural Documentation Gaps

Amazon's account review process during a suspension or compliance event often requires submitting:

- Articles of Organization / Certificate of Formation for the LLC

- EIN confirmation letter

- Beneficial ownership documentation (passport, proof of address)

- Bank statements showing the disbursement account

- Utility bills or other proof of business address

This is the moment when structural documentation gaps become visible. A foreign-owned LLC with a US address that is only the registered agent's address, a bank account that is on a fintech platform where statements are PDF exports from a web dashboard rather than traditional bank statements, and a beneficial owner whose proof of address is in a different country, presents an unusual documentation profile to Amazon's compliance reviewer. The seller may be fully compliant; the documentation simply doesn't match the typical pattern Amazon's reviewer is calibrated against.

For non-resident sellers, the structural mitigation is documentation maintained at formation: keep a clean record of the entity formation, EIN, banking onboarding, and operational presence. The bookkeeping considerations for cross-border founders cover the related question of operational records that align tax filings with bank activity.

Key Takeaways

- Amazon's account-linking detection runs on operational signals (IP, device, payment, banking, address, behavior, tax ID), not on legal entity names. A different LLC alone does not separate accounts.

- Enforcement is asymmetric: violations cascade across linked accounts; opening new accounts to escape enforcement compounds the risk.

- Foreign-owned US LLC Amazon sellers have two parallel IRS data tracks: the annual Form 5472 obligation regardless of Amazon activity, and Amazon's W-8BEN-E or 1099-K reporting depending on entity treatment.

- W-8BEN-E correctly filed shifts the 1099-K treatment for the seller, but the entity remains visible to the IRS through the W-8BEN-E record and through the LLC's separate Form 5472 filing.

- Multi-store strategy across separate LLCs works structurally only when every operational signal is separated. Same beneficial owner, same device, same banking, or same supplier defeats the separation.

- Through 2025 and into 2026 Q1-Q2, banking access for Amazon FBA sellers tightened at Mercury and Relay. Wise Business and Payoneer remain practical disbursement options for sellers without a verifiable US address.

References

- Form 1099-K — IRS

- About Form W-8 BEN-E — IRS

- About Form 5472 — IRS

- IRS Reporting Regulations on Third-Party Payment Transactions — Amazon Pay

- Amazon Seller Help — Multiple accounts policy

Related Reading

- Platform Risk: When Stripe or Wise Can Break You

- Form 5472: The $25K Penalty Chinese LLC Owners Miss

- What Happens If You Miss Form 5472 (Non-Resident LLC)

- Mercury vs Wise vs Relay for Non-Resident US LLC

- Wise vs Payoneer vs Mercury: Multi-Currency Compared

- Banking Redundancy Setup Guide

- Business Account Freeze Diagnostic

- Closing a Foreign-Owned US LLC: Dissolution + Final 5472

- Documentation Gap: What Authorities See

Disclosure

*Mercury is a fintech company, not an FDIC-insured bank. Banking services provided through Choice Financial Group and Column N.A., Members FDIC.

Related Tools

Related Articles

Closing a Foreign-Owned US LLC: Dissolution, Final 5472, and the EIN Reality (2026)

What closing a foreign-owned US LLC actually requires: state-level Articles of Dissolution, federal final Form 5472 + Pro Forma 1120 with Part V dissolution transactions, and the EIN closure letter. The structural reality of the 'do nothing' option.

Form 5472 for Chinese-Owned US LLCs: The $25K/Year Penalty (2026)

Chinese citizens with US LLCs file Form 5472 annually — the initial capital contribution alone triggers it. $25,000/year penalty, and paying a relative in China through the LLC means a second form.

Repatriating US LLC Profits to Mainland China: 5 Structural Paths Compared (2026)

Each path from a US LLC USD balance back to mainland China RMB produces a distinct compliance trail. Wise, PingPong / WorldFirst, OCBC intermediary, SAFE-registered personal channel, and USDT OTC — what each one looks like on the books, with the 2026 January-1 enhanced KYC overlay.

You Don't Need a CPA to File Taxes for Your US LLC (If You Have No Revenue Yet)

Zero-revenue, single-member, foreign-owned LLCs file Form 1120 plus Form 5472 by mail or fax. This is the structural workflow, the AI review step, and the thresholds where DIY stops being viable.

SBA Now Requires 100% Citizen Ownership for Loans -- What That Means for Cross-Border Founders

As of March 2026, SBA loans require 100% US citizen ownership. Green card holders, permanent residents, and mixed-citizenship businesses are now excluded. Here's what changed and why it matters structurally.

Summarize with AI

Cross-border entrepreneur running businesses across the US, China, and beyond for 20+ years. I built Global Solo to map the structural risks I wish someone had shown me.

Where does your structure have gaps?

Two free ways to map your cross-border risk — pick the depth that fits your time.

Structural Patterns

One blind spot, every two weeks. For entrepreneurs operating across borders.

Free LLC Formation Checklist included