How to Form a US LLC as a Non-Resident (2026 Complete Guide)

Step-by-step guide to forming a US LLC from outside the US — state selection, EIN, banking. What formation services cover and the 80% they don't.

Some links on this page go to partners who compensate us. This does not affect our analysis or rankings. How we make money

Every year, thousands of founders outside the US form an LLC. Pass-through taxation, limited liability, Stripe and PayPal compatibility, a real US bank account. If you're running a business from Lisbon or Bangkok, a US LLC unlocks infrastructure that most other entity types can't touch.

And the formation part is genuinely easy now. Pick a state, file articles of organization, get an EIN, open a bank account. Stripe Atlas, Firstbase, and Doola have turned the whole thing into a guided checkout flow.

I formed my first US entity from China in 2007, before any of these services existed. I faxed Form SS-4 to the IRS, waited weeks for an EIN, and found a registered agent through a lawyer referral. Today the mechanics are dramatically easier. But the gap between creating an entity and understanding what that entity requires of you hasn't changed at all.

Here's the problem: formation is maybe 20% of the work. The entity itself is real. The structure around it — tax position, compliance obligations, documentation across jurisdictions — often doesn't exist. That gap is where structural risk starts piling up.

This guide walks through each step, what each step actually establishes, and the 80% that formation doesn't address.

Why a US LLC: the structural case

A single-member LLC is a disregarded entity for US federal tax purposes. The entity doesn't pay income tax. Income passes through to the owner and gets taxed at the owner's personal rate, wherever they're tax resident. For non-resident aliens with no US-source income, this can mean zero US federal income tax on the LLC's earnings.

The multi-member trap. Everything above applies to single-member LLCs. Adding a second member — a co-founder, investor, or spouse — changes the LLC's tax classification entirely. A multi-member LLC defaults to partnership treatment under the IRS, requiring Form 1065 (US Return of Partnership Income) instead of the simpler Form 5472 + pro forma 1120. Partnership returns are significantly more complex, with separate Schedule K-1s for each member and different filing deadlines (March 15 vs. April 15). Tax practitioners report this as the most common structural mistake among non-resident founders — the assumption that all LLCs receive the same tax treatment regardless of member count.

That's the headline. But three other things matter just as much:

Limited liability. The LLC draws a legal line between your personal assets and the entity's obligations. How strong that line is depends on how you operate the entity after formation, not on the filing itself.

Banking and payment processor access. Stripe, PayPal, and most US processors require a US entity. An LLC with an EIN gets you into Mercury, Relay, Wise Business, and other neobanks that accept non-resident founders. See Mercury vs Wise vs Relay for a full comparison, and the Stripe vs Paddle vs Lemon Squeezy comparison for payment processor trade-offs including fee structure and tax handling. For many founders, banking access is the real reason they form the LLC.

Comparison with alternatives:

| Entity Type | Tax Treatment | Liability Protection | US Banking Access | Formation Complexity |

|---|---|---|---|---|

| US LLC (single-member) | Pass-through to owner | Yes | Full access | Low |

| US C-Corp | Corporate tax + dividend tax | Yes | Full access | Moderate |

| Home country entity | Varies by jurisdiction | Varies | Limited for US services | Varies |

| Estonian OU | Corporate tax on distribution | Yes | EU banking, limited US | Low-moderate |

A C-Corp pays its own income tax, then you pay again when profits are distributed. Unless you're raising venture capital, that double taxation usually makes no sense for a solo founder.

A home country entity works fine if you operate primarily in your own jurisdiction. But if you need US banking, US payment processors, or serve US-based clients, a foreign entity often can't get you there.

One thing worth being direct about: the US LLC is not inherently better. It fits a specific situation — cross-border operations that depend on US financial infrastructure. If that's not your situation, you may not need one.

Step by step: state selection

US LLCs are formed at the state level. For non-residents, three states dominate: Delaware, Wyoming, and New Mexico.

State comparison

| Factor | Delaware | Wyoming | New Mexico |

|---|---|---|---|

| Formation fee | $90 | $100 | $50 |

| Annual fee / franchise tax | $300/year | $60/year | $0 |

| Privacy (member names public?) | No | No | No |

| State income tax on LLC | None for non-residents | None | None for non-residents |

| Court system | Chancery Court (specialized) | Standard | Standard |

| Registered agent required | Yes | Yes | Yes |

| Typical use case | Venture-backed, investor-expected | Solo founders, cost-conscious | Lowest cost formation |

Delaware is the default everyone talks about. Its Chancery Court specializes in business disputes, and its corporate law is the most developed in the US. For C-Corps raising venture capital, Delaware is the standard. For single-member LLCs operated by non-residents, the main advantage is familiarity: formation services default to it, banks never blink. The downside is cost — $300/year in franchise tax, the highest of the three.

Wyoming is the sweet spot for most solo founders. No state income tax, $60/year annual report, strong asset protection. If you don't anticipate investor scrutiny, Wyoming gives you the same legal protection as Delaware at a fraction of the ongoing cost.

New Mexico is the cheapest option — zero annual fees, zero franchise tax. The trade-off: some neobanks process New Mexico LLCs more slowly or request extra documentation. The legal protection is identical. The practical friction during banking setup may not be.

For a solo non-resident LLC, the state of formation barely affects legal protection or tax treatment. The real differences are cost and how smoothly the next steps (especially banking) go. None of these states tax LLC income earned by non-residents from out-of-state sources.

How does your structure score?

Free 2-minute screening across Money, Entity, Tax, and Accountability.

Registered agent: what it is and why you need one

Every US LLC needs a registered agent in its state of formation — a person or entity with a physical address in that state, authorized to receive legal documents on behalf of the LLC.

If you let the registered agent lapse, the state can dissolve your entity. For non-residents with no US presence, a commercial registered agent is the only practical option. For a broader look at how state selection interacts with agent costs and other ongoing fees, see the best state for non-resident LLCs guide.

What a registered agent does:

- Receives service of process (lawsuits, legal notices)

- Receives official state correspondence (annual report notices, tax notices)

- Forwards everything to your mailing address

What a registered agent does not do:

- File taxes or annual reports

- Keep your LLC in compliance

- Give legal or tax advice

You'll likely also need a US mailing address for banking and IRS correspondence. That's a separate service. See the virtual mailbox comparison for options.

Commercial registered agents run $50-$300/year. Northwest, Incfile, and ZenBusiness offer standalone service. Stripe Atlas, Firstbase, and Doola bundle a registered agent into their formation packages, though sometimes only for the first year.

Watch the renewal. A lapsed registered agent can cascade fast: loss of good standing, banking problems, payment processor shutdowns, inability to file required documents. This is a recurring obligation, not a one-time checkbox.

EIN application: the process for non-residents

An EIN (Employer Identification Number) is the entity's tax ID, issued by the IRS. You need it for bank accounts, tax returns, and payment processors. US residents can get one online in minutes. Non-residents cannot.

If you don't have an SSN or ITIN, the IRS online application won't work. Your options:

-

Fax: Complete Form SS-4, fax it to the IRS. Expect 4-6 weeks, sometimes longer.

-

Phone: Call the IRS Business & Specialty Tax Line with Form SS-4 information ready. You get the EIN on the call. Fastest method, but you're dealing with IRS hold times during Eastern Time business hours.

-

Third-party services: Formation services and registered agents often handle this as part of their package. Some use the phone method and deliver within days. Others fax and take weeks.

Common problems:

-

Responsible party identification. Form SS-4 requires a "responsible party" — the person who controls the entity. For a single-member LLC, that's you. The IRS wants a foreign address if the responsible party isn't in the US.

-

ITIN confusion. You do not need an ITIN to get an EIN. The EIN is for the entity; the ITIN is for you personally. Some formation services mix these up, creating delays that don't need to exist.

-

Fax failures. The IRS fax system loses faxes. There's no confirmation of receipt. Following up means calling the IRS, which means more hold times.

-

Name matching. The name on Form SS-4 must exactly match the entity name on the state filing. Even minor punctuation differences can cause rejection.

Without an EIN, the LLC can't open a bank account, accept payments through US processors, or file taxes. For most non-residents, this is the biggest bottleneck in the entire formation process.

Banking as a non-resident: opening the account

LLC formed, EIN in hand. Now you need a bank account. For non-residents, that means neobanks with remote account opening.

| Factor | Mercury | Relay | Wise Business |

|---|---|---|---|

| Entity requirement | US LLC or Corp | US LLC or Corp | Varies (multi-entity) |

| In-person required | No | No | No |

| Currencies | USD | USD | Multi-currency (50+) |

| FDIC insured | Yes (via partner banks) | Yes (via partner banks) | Not FDIC; safeguarded funds |

| International transfers | Via wire transfer | Via wire transfer | Native multi-currency |

| Integrations | Extensive (QuickBooks, etc.) | Good (QuickBooks, Xero) | Limited |

| Interest on deposits | Yes (Treasury) | No | Yes (some currencies) |

| Typical approval time | 1-5 business days | 1-5 business days | 1-3 business days |

Mercury is where most non-resident LLC founders end up. Application is online: Articles of Organization, EIN confirmation letter, government ID, business description. Be aware that Mercury has been tightening its review process. Non-resident applications for newly formed entities with no revenue history increasingly get flagged for additional documentation.

Relay has a comparable process but fewer non-resident founders use it. Its profit-first banking categories and team management features are more relevant if you have employees or contractors.

Wise Business is different entirely. Wise isn't a bank — it's an electronic money institution. No FDIC insurance, but native multi-currency support across 50+ currencies. You get local bank details in multiple countries, which makes receiving international payments simpler. For founders who move money across borders constantly, Wise often makes more sense than a USD-only account.

What triggers extra banking scrutiny:

- Brand-new entity with no operating history

- Beneficial owner in certain jurisdictions

- Transaction patterns that don't match the declared business purpose

- Heavy international transfers relative to domestic activity

- Mismatches between the application and publicly available information

Approval is not guaranteed. KYC and AML checks evaluate the entity, the beneficial owner, and the business purpose. Rejection happens. Having clear documentation of what the business does and how it generates revenue helps, but doesn't eliminate the risk.

See Business Account Freeze Diagnostic for what happens when banking goes wrong.

What formation services cover vs what they don't

Formation services have turned LLC creation into a product. Here's what each one actually includes:

| Feature | Stripe Atlas | Firstbase | Doola | DIY |

|---|---|---|---|---|

| Entity type | C-Corp (default) | LLC or C-Corp | LLC or C-Corp | Any |

| State | Delaware | Delaware or Wyoming | Wyoming or Delaware | Any |

| Articles of Organization/Incorporation | Included | Included | Included | You file |

| EIN | Included | Included | Included | You apply |

| Registered agent | Included (1 year) | Included | Included | You arrange |

| Operating agreement | Template | Template | Template | You draft |

| Bank account | Mercury/SVB | Partner banks | Partner banks | You apply |

| 83(b) election (C-Corp) | Template | N/A | N/A | N/A |

| Bookkeeping | No | No | Add-on | No |

| Tax filing | No | No | Add-on | No |

| Compliance calendar | No | No | Partial | No |

| Cost | $500 | $399-599 | $297-597 | $50-200 |

Stripe Atlas defaults to a Delaware C-Corp, not an LLC. If you're a solo founder with no plans to raise venture capital, a C-Corp saddles you with corporate income tax the LLC avoids. Atlas now supports LLCs, but the default path and most documentation still assume C-Corp.

Firstbase is more flexible on entity type and state, and the product is built specifically for non-US founders.

Doola goes further than the others on ongoing compliance. Bookkeeping and tax filing add-ons are available, which matters if you don't have access to a US-based accountant.

See Stripe Atlas vs Firstbase vs DIY for a deeper comparison, and the full pricing breakdown across Doola, Firstbase, and Stripe Atlas for 3-year cost projections.

The common thread: all of these services create an entity. None of them create a structure. You get a name, a state registration, a tax ID, and a registered agent. How that entity interacts with your tax residency, what reporting obligations it triggers, what documentation you need to maintain the arrangement — none of that is in scope.

The 80% formation doesn't cover

Formation handles roughly 20% of a cross-border founder's structural position. The rest exists independently of how the entity was created, and none of it shows up in any formation service's workflow.

Tax residency interaction. LLC income passes through to you. Where you're tax resident determines where that income is taxed. If you're tax resident in Germany with a Wyoming LLC, Germany taxes that income. Formation does nothing to assess or document this relationship. See Digital Nomad Tax Residency Guide 2026 for how tax residency actually works across jurisdictions.

FBAR and FATCA reporting. US persons (citizens, permanent residents) who own or control foreign accounts exceeding $10,000 aggregate balance at any point during the year must file an FBAR (FinCEN Form 114). Non-US persons who own a US LLC may have FATCA obligations depending on their country's agreement with the US. These obligations attach to the person, not the entity.

Permanent establishment risk. If you operate a US LLC while living and working in another country, you may create a permanent establishment for the LLC in that country. That can trigger corporate tax obligations on top of your personal income tax. The PE risk analysis explains how this works in practice. Whether PE applies depends on your activities, the US tax treaty with your country of residence, and local law.

Transfer pricing. If you run multiple entities — say, a US LLC and a home country company — you need documentation supporting the pricing of transactions between them under OECD guidelines. Without it, tax authorities on either side can reclassify income, and you end up double-taxed. See Transfer Pricing for One-Person Companies. Formation services create individual entities. They don't document the relationship between them.

Compliance calendar. Annual report filings, franchise tax payments (Delaware), registered agent renewals, BOI reporting. The cross-border compliance checklist maps every recurring obligation with deadlines. Miss them and you're looking at penalties, loss of good standing, banking freezes. Formation services may send reminders. They don't manage any of it.

Operating agreement adequacy. Every formation service gives you a template operating agreement. For a single-member LLC, it's usually generic boilerplate that doesn't reflect how the business actually runs. After a year of operations, the template almost never matches reality. That mismatch weakens the legal foundation of the entity's separate identity.

What this means for your structure

Forming a US LLC as a non-resident is mechanically straightforward. The services are mature, the timeline is days or weeks, and the entity you get is real — banking access, payment processor compatibility, liability protection.

The gap is between what formation creates and what your cross-border situation actually requires. Formation gives you an entity. Your structural position includes that entity plus your personal tax residency, the jurisdictions you operate in, the reporting obligations triggered by the combination, and the documentation tying it all together.

No formation service fills this gap. Not because they're failing at their job, but because the gap sits at a different level — where entity structure meets personal circumstance meets multi-jurisdictional obligations.

I've watched this play out dozens of times: a founder forms the LLC in a weekend, gets the bank account, starts processing payments, and then 14 months later discovers the compliance obligations they've been ignoring since day one. Formation is the first step in a position that extends well beyond it. The real structural questions start the day after you file.

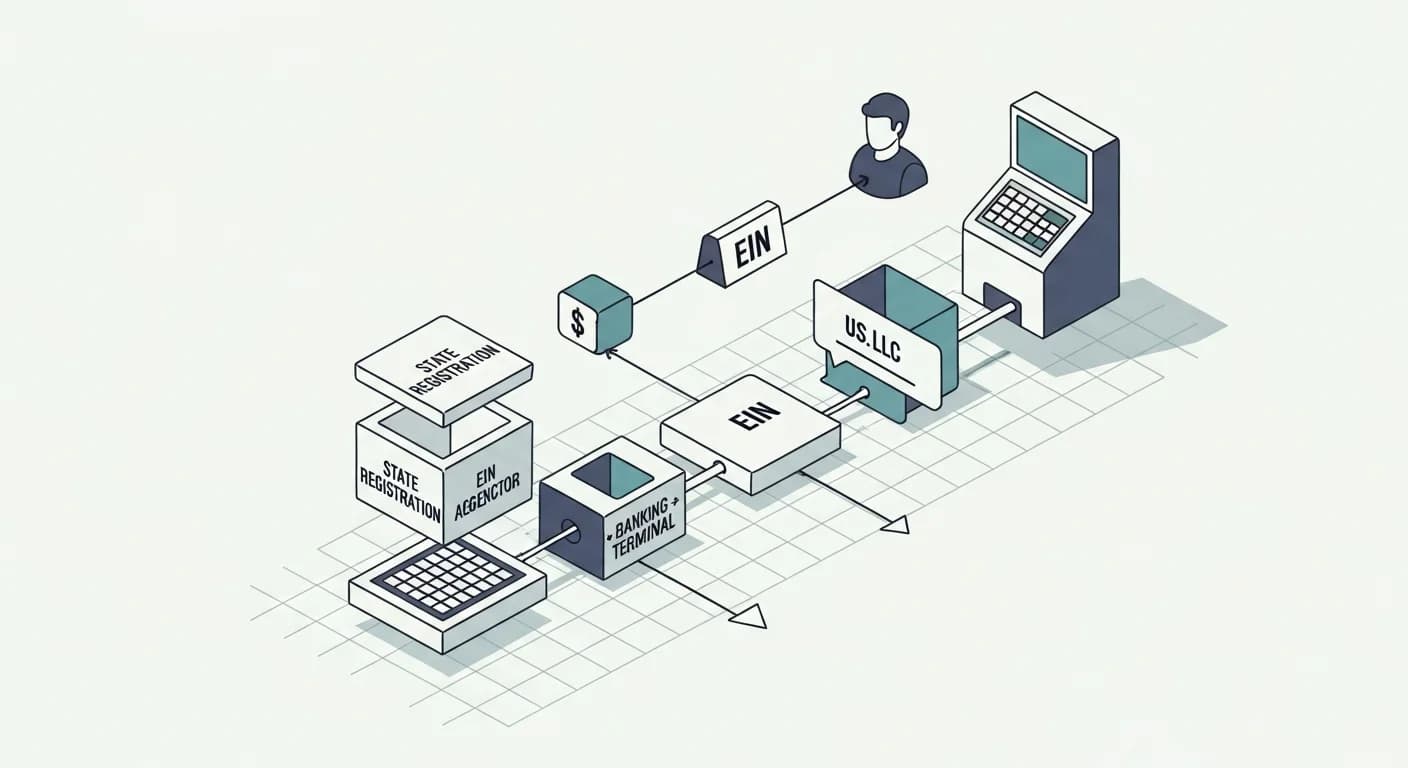

Visual: LLC Formation Process and Structural Gap

| Stage | Detail | Risk |

|---|---|---|

| State Selection | DE / WY / NM | Low |

| Registered Agent | Commercial Service | Low |

| Articles Filed | Entity Created | Low |

| EIN Application | Form SS-4 | Low |

| Banking Setup | Mercury / Wise / Relay | Low |

| ── Formation Ends Here ── | — | |

| Tax Position | Residency + Pass-Through, Interaction | High |

| Compliance | FBAR / FATCA / PE Risk, BOI Reporting | High |

| Documentation | Operating Agreement, Transfer Pricing, Compliance Calendar | High |

FAQ

Can a non-US resident form an LLC without visiting the United States?

Yes. State filing, EIN application, registered agent setup, bank account opening — all of it can be done remotely. Stripe Atlas, Firstbase, and Doola handle the process online. DIY means filing directly with the state and faxing Form SS-4 to the IRS.

Do I need an SSN or ITIN to form a US LLC?

No. The EIN application (Form SS-4) for foreign-owned single-member LLCs is filed by fax or phone. The EIN goes to the entity, not to you. An ITIN may come up later for certain tax filings, but it's not needed for formation or banking.

Which state is best for a non-resident LLC — Delaware or Wyoming?

For solo non-resident LLCs, the state barely affects legal protection or tax treatment. Wyoming: $100 to form, $60/year. Delaware: $90 to form, $300/year. Unless you're raising venture capital (where Delaware's Chancery Court matters), Wyoming is cheaper with equivalent protection.

What does LLC formation not cover for cross-border founders?

Formation creates a legal entity — roughly 20% of the picture. The other 80%: tax residency determination, FBAR and FATCA reporting, permanent establishment risk, transfer pricing documentation, the ongoing compliance calendar (annual reports, franchise taxes, registered agent renewals), and operating agreement adequacy.

How long does it take to get an EIN as a non-resident?

By phone: immediate (on the call). By fax: 4-6 weeks, sometimes longer. Formation services using the phone method deliver within days. The online application is not available without an SSN or ITIN.

Key Takeaways

- The US LLC works well for cross-border solo founders who need US financial infrastructure. It's not universally optimal — it fits a specific situation.

- State selection (Delaware, Wyoming, New Mexico) barely matters for legal protection or tax treatment. The real differences are cost and banking friction.

- The EIN is the biggest bottleneck for non-residents. No SSN or ITIN means no online application — you're stuck with fax or phone.

- Formation services create an entity. They don't create a structure. Tax position, compliance, PE risk, and documentation are all on you.

- The 80% that formation doesn't cover — tax residency, FBAR/FATCA, permanent establishment, transfer pricing, compliance calendar — starts accumulating the day the entity is formed.

References

- IRS: Apply for an Employer Identification Number (EIN) Online — IRS EIN application process and Form SS-4 instructions

- Wyoming Secretary of State: LLC Formation — Wyoming LLC formation requirements and filing process

- IRS: Classification of Taxpayers for U.S. Tax Purposes — IRS guidance on entity classification and pass-through treatment

- FinCEN: Beneficial Ownership Information Reporting — BOI reporting requirements under the Corporate Transparency Act

- IRS Form SS-4: Application for Employer Identification Number — EIN application form and instructions for domestic and foreign applicants

- Delaware Division of Corporations — Delaware entity formation requirements and annual franchise tax obligations

- OECD: Permanent Establishment — International framework for PE determination under tax treaties

- IRS: Single Member Limited Liability Companies — Federal tax treatment of disregarded entities

- Stripe Atlas — Formation service for C-Corps and LLCs with integrated banking

Disclosure

*Mercury is a fintech company, not an FDIC-insured bank. Banking services provided through Choice Financial Group and Column N.A., Members FDIC.

META — Entity

Entity — Structure & Formation — 22 articlesRelated Tools

Related Articles

SBA Now Requires 100% Citizen Ownership for Loans -- What That Means for Cross-Border Founders

As of March 2026, SBA loans require 100% US citizen ownership. Green card holders, permanent residents, and mixed-citizenship businesses are now excluded. Here's what changed and why it matters structurally.

US LLC vs C-Corp for Non-Residents: Which Entity Type?

LLC pass-through vs C-Corp double taxation, governance, VC eligibility, and compliance costs, mapped for non-resident founders choosing a US entity.

BOI Filing: Do Non-Resident LLC Owners Need to File?

FinCEN's March 2025 rule exempted US-formed LLCs from BOI filing. Who is exempt, who still files, and what the transparency trend means.

Do I Need a US LLC? Non-Resident Decision Framework (2026)

A US LLC costs $500-1,500/yr to maintain. When it creates real value vs unnecessary complexity — and the alternatives most founders overlook.

BEA-15: The Federal Survey Most LLC Owners Miss

Foreign-owned US LLCs may owe a BEA-15 filing to the Bureau of Economic Analysis. Who files, exemptions, deadlines, and how it differs from Form 5472.

Summarize with AI

Cross-border entrepreneur running businesses across the US, China, and beyond for 20+ years. I built Global Solo to map the structural risks I wish someone had shown me.

Where does your structure have gaps?

Two free ways to map your cross-border risk — pick the depth that fits your time.

Structural Patterns

One blind spot, every two weeks. For entrepreneurs operating across borders.

Free LLC Formation Checklist included