First Year Cross-Border Founder: Every Decision Map

LLC or sole prop? Which state? Bank where? Month-by-month map of every structural decision cross-border founders face in year one.

Some links on this page go to partners who compensate us. This does not affect our analysis or rankings. How we make money

Your first year running a cross-border business sets precedent that sticks. The entity you form, the bank you open, the way income flows, how you file taxes, what you document -- these choices compound. Every future action builds on them or pays to undo them.

Most founders treat year one as a series of independent problems. Form an entity. Open a bank account. Get paid. File taxes. Solve each one as it comes up, in whatever order feels most urgent. But these decisions are not independent. They form a dependency chain. The first choice constrains the second, the second constrains the third, and by month twelve the accumulated constraints define how your business actually operates.

What follows is a structural map of how those decisions interact, what depends on what, and what happens when you leave the sequence to chance.

Month 1-2: The foundation decisions

Three decisions in the first two months set the foundation. They interact, and the order matters.

Tax residency position. Where are you, and where does each jurisdiction believe you to be? This is the anchor. It determines which country taxes your worldwide income, which treaties apply, and what compliance obligations follow.

I've seen this backwards more times than I can count: founders form a US LLC first, then discover the entity creates obligations they never anticipated in jurisdictions they didn't expect. Tax residency is almost always the last thing addressed. It should be the first.

The question isn't "where do I want to be tax resident?" It's "where do each country's rules say I am, given my actual facts?" The tax residency determination guide maps how different countries answer this using different criteria.

Entity formation. LLC, C-Corp, home country entity, or nothing at all. Each creates a different structural position: different liability boundaries, tax treatment, banking options, compliance load. The entity decision framework maps these trade-offs.

A US LLC owned by a non-resident creates different obligations than the same LLC owned by a US tax resident. An Estonian OU creates local corporate tax obligations a Wyoming LLC does not. A sole proprietorship creates no entity boundary at all, so income classification, liability, and documentation all flow through you personally.

The entity cannot be properly evaluated without the residency position, because the entity's tax treatment depends on where the owner is tax resident. Forming the entity first and sorting residency later is backwards. The entity structure analysis covers why the LLC question is structural, not purely tax-driven.

Banking setup. Which bank, which jurisdiction, which account type. See Mercury vs Wise vs Relay for a comparison of the major options. Banking is constrained by entity type and jurisdiction. A US LLC can open a US business bank account; a sole proprietor operating internationally faces different options. A non-resident founder encounters different requirements and ongoing compliance than a resident one. Once opened, the bank account becomes the conduit for all revenue, and banks apply their own risk models to the transaction patterns they see.

Residency, entity, banking. Each constrains the next. When these are made in reverse order or without reference to each other, you end up with a foundation built on assumptions that may not hold.

Month 3-4: Income architecture

Foundation decisions are in place (or, more commonly, half in place). Revenue starts flowing. The decisions you make now establish how money enters the business and how it gets classified.

Payment processing setup. Stripe, Wise, PayPal, direct bank transfer. Your processor choice determines the currencies available, countries served, fee structure, and documentation generated. A Stripe account connected to a US LLC and US bank creates a specific income trail -- one Stripe reports to the IRS via 1099-K. A Wise Business account creates a different trail. See Stripe vs Paddle vs Lemon Squeezy for processor trade-offs. Your processor isn't just a payment tool. It's a documentation system generating records visible to tax authorities, banks, and compliance reviewers.

First client contracts. Your first invoice does more than bill a client. It establishes a pattern. How the service is described, the currency used, the entity name on the invoice, the tax treatment applied -- all create precedent. The invoice trail analysis shows how a single invoice can be classified differently across jurisdictions, with cascading implications for withholding.

Income classification. Service income, royalty income, management fee, or something else? The classification isn't always within your control -- the source country may classify it differently than the residence country. But how you set up invoicing, describe your services, and structure contracts influences the initial characterization. And that characterization tends to stick, because changing it later means explaining the change to tax authorities, banks, clients, and platforms.

The income architecture you build in month 3-4 creates a trail that feeds into tax filings, bank histories, and compliance records. Changing the architecture later doesn't erase that trail. It creates a discontinuity that invites examination.

How does your structure score?

Free 2-minute screening across Money, Entity, Tax, and Accountability.

Month 5-6: Documentation baseline

By month five you have a foundation (entity, bank, residency position) and an income architecture (processor, contracts, classification). What you probably don't have is documentation tying it all together.

Operating agreement. For an LLC, this defines how the entity operates, how profits are distributed, and what the owner's relationship to the entity is. Most single-member LLC founders skip it or use a minimal template. Bad idea. The operating agreement defines the entity's substance. Without it, the entity exists as a registered filing but has no internal documentation proving it operates as a separate business.

Contractor agreements. If you engage contractors -- designers, developers, writers, virtual assistants -- the agreements establish how those relationships are classified. The contractor classification analysis covers how misclassification creates structural risk. No written agreement doesn't prevent the relationship from existing. It prevents you from documenting what the relationship actually is. Tax authorities in multiple jurisdictions examine contractor relationships, and the paperwork (or lack of it) is the primary evidence.

Transfer pricing documentation. If you operate through multiple entities -- say a US LLC and a home country entity -- the pricing of transactions between them carries tax implications. Transfer pricing rules apply to intercompany transactions, and the documentation establishing arm's-length pricing is expected to exist from the start, not reconstructed retroactively.

Bookkeeping system. Revenue in, expenses out, categorized and reconciled. The system you set up in months 5-6 creates the record your tax filings will be based on. The documentation analysis describes a gap I see constantly: founders treat bank statements and Stripe dashboards as their bookkeeping. That gives you raw transaction data but not the categorization, reconciliation, and documentation a tax preparer or examiner actually needs.

The documentation baseline doesn't need to be complex. It needs to exist. Each document you create now supports the structural position you've built (intentionally or not) in months 1-4. Each gap becomes harder to fill as time passes and memory fades.

Month 7-9: First compliance events

Revenue is flowing and the first external compliance events arrive. This is where the structural position you built in months 1-6 meets institutional examination for the first time.

Quarterly estimated taxes. In the US, estimated tax payments are due quarterly (April 15, June 15, September 15, January 15). If you formed a US LLC and are US tax resident, or if you're a US citizen abroad, estimated tax obligations start in the first year of income. Miss them and penalties compound. The first estimated payment is also the first moment where your income classification, entity structure, and tax position get translated into a dollar amount owed to a specific jurisdiction.

State compliance. US LLCs have state-level obligations that vary by formation state and operation state. Annual reports, franchise taxes, registered agent fees. California imposes a minimum franchise tax of $800 regardless of revenue. Form a Delaware LLC but have nexus in California? You may owe franchise tax in both. The cross-border compliance checklist inventories every state and federal filing obligation. The state compliance environment is fragmented, and obligations aren't always obvious from formation documents.

Banking review triggers. Banks conduct periodic reviews of account activity. Revenue milestones or unusual transaction patterns trigger enhanced due diligence. An account receiving $2,000/month that suddenly gets $25,000 in one month will generate an inquiry. The bank isn't judging your business. It's applying risk models to transaction patterns. Your ability to respond depends entirely on the documentation baseline from months 5-6. If that baseline is thin, the inquiry gets stressful and the response gets improvised.

Platform reporting. Payment processors generate tax reporting documents -- 1099-K in the US, equivalent forms elsewhere. These go to both you and the tax authority. The amounts are expected to match your own filings. Discrepancies between what the platform reports and what you file create examination triggers that can surface months or years later.

None of this is new obligations being created. These are the structural consequences of months 1-6 becoming visible to external parties for the first time.

Month 10-12: Year-end structural review

The final quarter is where the accumulated decisions either cohere into a defensible position or reveal gaps that will haunt year two.

Year-end tax position assessment. Total taxable income. Which jurisdictions. Which classification. What documentation supports it. If the preceding months didn't generate the records, these questions can't be answered quickly. Clean bookkeeping and documented entity substance let you assess your position efficiently. A pile of bank statements and a Stripe dashboard means a reconstruction exercise that's both slow and uncertain.

S-Corp election window. For US LLCs with sufficient income, electing S-Corp tax treatment can affect self-employment tax. See S-Corp Election Timing for when the election is and isn't structurally favorable. The election can be made retroactively for the current tax year if filed by March 15 (Form 2553), but evaluating whether it's beneficial requires understanding the full year's income. Which brings you right back to the documentation baseline. This window opens briefly and closes firmly.

FBAR assessment. US persons (citizens, residents, green card holders) with foreign financial accounts exceeding $10,000 in aggregate at any point during the year have FBAR filing obligations (FinCEN Form 114). Low threshold, high penalties, April 15 deadline (auto-extended to October 15). A cross-border founder with bank accounts in multiple countries may trigger FBAR obligations without realizing it. The assessment requires knowing every financial account held at any point during the year, including accounts opened and closed, accounts with signatory authority, and accounts that briefly exceeded the threshold. More on common traps in FBAR for Digital Nomads.

State nexus evaluation. By year's end, your activity pattern may have created nexus -- a taxable connection -- in states beyond where you formed your entity. Sales into certain states, contractors in certain states, physical presence in certain states. The question is whether the year's activity created obligations you didn't anticipate at formation.

The year-end review is the first time you can see the full picture. Founders who do this review before the tax year closes have the most options. Those who wait face fewer.

Decision dependencies: what constrains what

The month-by-month timeline obscures something important: these decisions have hard dependencies. The sequence is not arbitrary.

Tax residency before entity. The entity's tax treatment depends on where the owner is tax resident. Form the entity first and you're forced to resolve residency retroactively, which creates a period of structural ambiguity.

Entity before banking. US banks require entity documentation (articles of organization, EIN) to open a business account. Entity type determines which banks will accept you and on what terms.

Banking before payment processing. Processors need a bank account to connect to. The bank's jurisdiction and type constrain which processors work and how funds settle.

Payment processing before first revenue. Revenue can't flow until the processing infrastructure exists. This creates time pressure that drives the whole sequence -- founders make entity and banking decisions fast because they need to get paid, not because they've thought through the chain.

Documentation before compliance events. Tax filings, estimated payments, and bank inquiries all require documentation that existed before the event. Not documentation created in response to it.

The chain runs: residency, entity, banking, processing, revenue, documentation, compliance. Each step depends on the one before. Skipping steps or completing them out of order doesn't eliminate the dependencies. It creates gaps that surface at the compliance stage.

The cost of winging it

The most common first-year approach is no approach at all. You form an entity because Stripe requires one. Open a bank account because the entity needs one. Start invoicing because clients are waiting. File taxes because the deadline arrives. Every decision is reactive, driven by the immediate need, not by its position in the chain.

This produces default positions that emerge from the sequence of reactions rather than from deliberate choices.

Default entity. Whatever was fastest to form. Usually a Delaware or Wyoming LLC because a formation service suggested it. The LLC formation guide covers what formation services handle and the 80% they leave unaddressed, and the formation service pricing comparison shows how year-one costs differ from three-year totals. The entity may or may not match your tax residency position, income profile, or long-term structure.

Default banking. Whatever bank would open an account for the entity type you picked. Limitations on international transfers, multi-currency transactions, or account activity only become apparent later.

Default tax position. Whatever the first filing establishes. File as a sole proprietor on Schedule C and that classification creates precedent. Skip estimated taxes and penalties start accumulating. Miss FBAR and the non-filing itself becomes a gap that persists.

Default documentation. Whatever you happen to have. Bank statements, yes. Stripe dashboard, yes. Operating agreement, probably not. Contractor agreements, probably not. Travel log, almost certainly not.

The structural debt from default positions works like technical debt in software: the system still runs, but the cost and risk of every future change goes up. Restructuring an entity with twelve months of contracts, bank history, tax filings, and processor relationships attached is a completely different exercise from choosing the right entity on day one. The timing trap analysis covers how deferral itself becomes a dependency -- each month under default positions adds another layer that increases the eventual cost of correction.

This pattern holds across cross-border founders I've worked with: structural decisions cost the least when made deliberately and in sequence, and the most when made reactively and out of order. Year one creates the reality that everything after either builds on or pays to change.

What this means for your structure

The first-year decision map isn't about making perfect decisions. In a cross-border environment, perfect is rarely knowable in advance. It's about recognizing that decisions are interconnected, sequence matters, and defaults created by inaction carry the same structural weight as deliberate choices.

The question at the end of year one isn't whether every decision was optimal. It's whether the dependency chain is visible, the documentation baseline exists, and the positions you've taken are ones you can defend -- or at minimum, have consciously acknowledged.

Year one creates the precedent. Everything after either reinforces it or pays to change it.

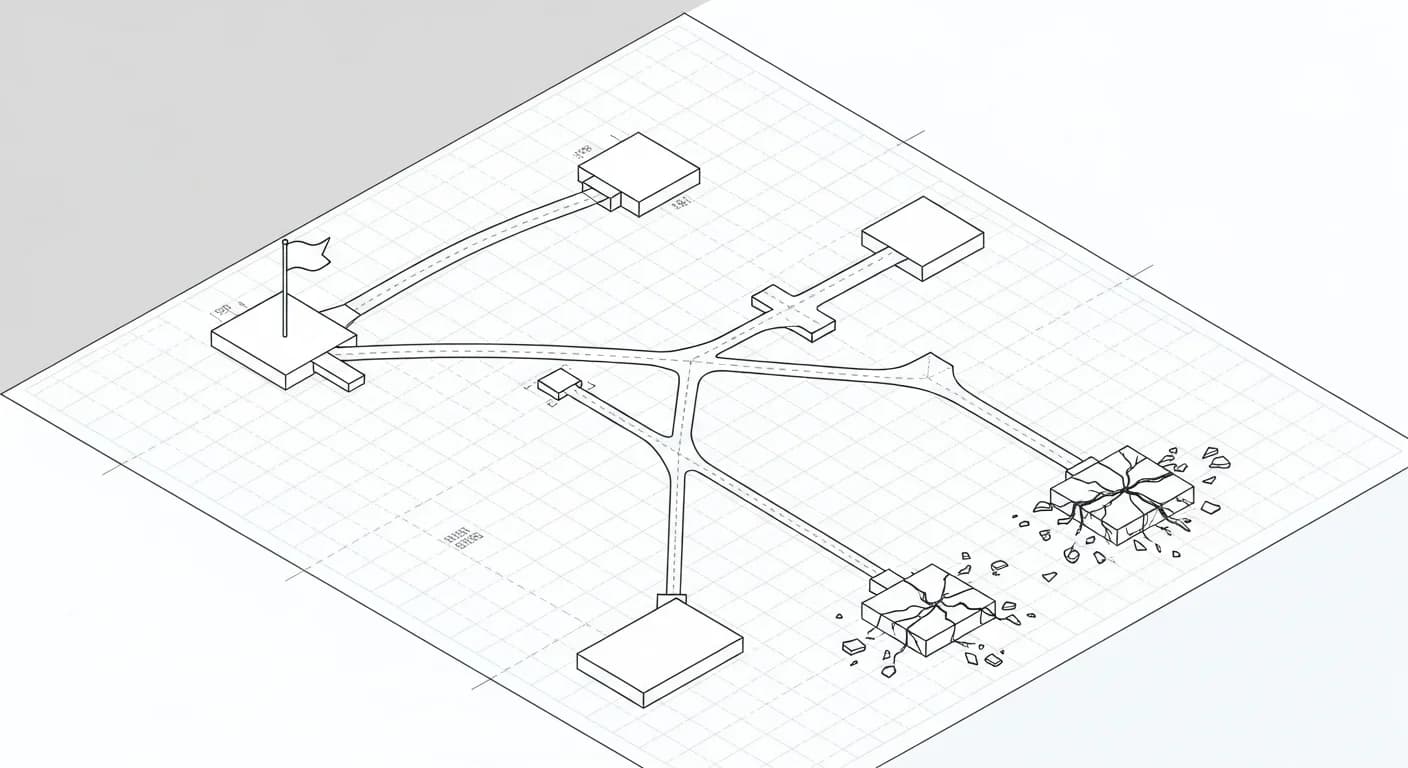

Visual: First-Year Decision Timeline

| Stage | Detail | Risk |

|---|---|---|

| Month 1-2 | Foundation | — |

| Tax Residency | Position | Medium |

| Entity | Formation | Medium |

| Banking | Setup | Medium |

| Month 3-4 | Income Architecture | — |

| Payment | Processing | — |

| First Client | Contracts | — |

| Month 5-6 | Documentation | — |

| Operating Agreement | + Bookkeeping | — |

| Month 7-9 | Compliance Events | — |

| Estimated Taxes | + Banking Review | Medium |

| Month 10-12 | Year-End Review | — |

| Year-End Assessment | S-Corp Window, FBAR Check | Medium |

| No Deliberate | Sequence → Default, Positions Accumulate | High |

FAQ

What is the first structural decision a cross-border founder needs to make?

Tax residency. It constrains entity choice, entity constrains banking, banking constrains payment processing. Forming a US LLC before understanding tax residency implications creates gaps that surface during compliance events.

Can I figure out my cross-border structure as I go?

You can try, but deferral creates default positions that compound. Every month invoicing without an entity creates sole proprietor income classification. Every month of banking without documentation creates audit trail gaps. Every quarter without estimated tax payments creates penalty exposure. Fixing these in month twelve costs far more than addressing them in month one.

What mistakes do first-year cross-border founders make most often?

Forming an entity in the wrong jurisdiction (US LLC when no US banking or client need exists). Choosing a state based on marketing rather than fit (Delaware when Wyoming is cheaper with equivalent protection — see the best state for non-resident LLC guide). Opening only one bank account (single point of failure). Ignoring tax residency until the first filing deadline. Each creates path dependency that's expensive to unwind.

What compliance obligations start immediately after forming an LLC?

From day one: registered agent must be maintained (or the entity risks dissolution), annual report and franchise tax obligations begin accruing (due dates vary by state), Form 5472 is required annually for foreign-owned LLCs ($25,000 penalty for non-filing), and estimated tax payments may be due quarterly depending on tax residency. Banking KYC reviews also become ongoing.

Key Takeaways

- Year one creates a dependency chain: tax residency constrains entity choice, entity constrains banking, banking constrains payment processing. Decisions made out of sequence create structural gaps that surface during compliance events.

- Tax residency is the first decision that matters, but commonly the last one addressed. Forming an entity before clarifying residency can create obligations in jurisdictions you didn't expect.

- The documentation baseline from months 5-6 (operating agreement, contractor agreements, bookkeeping) determines how well you can respond to first compliance events in months 7-9. Documentation created retroactively is weaker than documentation that existed at the time.

- Default positions from reactive decisions -- whatever entity was fastest, whatever bank would open an account, whatever the first filing established -- carry the same structural weight as deliberate choices and accumulate debt that increases the cost of every future change.

- Structural correction costs the least when decisions are made deliberately and in sequence during year one. Each month under default positions adds another layer. The first year creates precedent that everything after either builds on or pays to change.

References

- IRS: Estimated Taxes — Quarterly estimated tax payment requirements and deadlines for US taxpayers

- FinCEN: FBAR Filing Requirements — Foreign Bank Account Report obligations for US persons with foreign financial accounts

- IRS Form 2553: S Corporation Election — S-Corp election requirements, deadlines, and eligibility criteria

- Delaware Division of Corporations — Delaware entity formation requirements and annual compliance obligations

- Wyoming Secretary of State: Business Formation — Wyoming LLC formation and annual report requirements

- IRS: Substantial Presence Test — Determining US tax residency based on physical presence

- IRS Tax Treaties — US bilateral tax treaties affecting cross-border founders

Disclosure

*Mercury is a fintech company, not an FDIC-insured bank. Banking services provided through Choice Financial Group and Column N.A., Members FDIC.

META — Accountability

Accountability — Documentation & Audit Readiness — 13 articlesRelated Tools

Related Articles

Hiring in India: Contractor vs EOR vs Entity (US LLC, 2026)

How a non-resident US LLC hires its first person in India: contractor vs EOR vs own entity, and the misclassification, payroll, tax, and PE layers underneath.

Do You Need an ITIN to Get a US Credit Card? (2026)

An ITIN will not get you a US credit card on its own, and for paying for AI tools it is the wrong tool. What the IRS requires, and what works instead.

US LLC for Bali Digital Nomads: The 183-Day Tax Guide (2026)

Run a US LLC from Bali? Indonesia's 183-day residency rule is the pivot: worldwide-income tax, CRS vs FATCA visibility, and banking, mapped for nomads.

Repatriating US LLC Profits to Mainland China: 5 Structural Paths Compared (2026)

Each path from a US LLC USD balance back to mainland China RMB produces a distinct compliance trail. Wise, PingPong / WorldFirst, OCBC intermediary, SAFE-registered personal channel, and USDT OTC — what each one looks like on the books, with the 2026 January-1 enhanced KYC overlay.

What to Check After Filing Your US LLC Taxes: A Post-Filing Structural Review (2026)

You filed. You made the deadline. Here are the five structural checks most cross-border LLC founders skip in the 30-60 days after April 18 — and why filing compliance is not the same as structural correctness.

Summarize with AI

Cross-border entrepreneur running businesses across the US, China, and beyond for 20+ years. I built Global Solo to map the structural risks I wish someone had shown me.

Where does your structure have gaps?

Two free ways to map your cross-border risk — pick the depth that fits your time.

Structural Patterns

One blind spot, every two weeks. For entrepreneurs operating across borders.

Free LLC Formation Checklist included